TA-Lib, Technical Analysis Library は 2001 年にリリースされ、20 年以上経った今でも広く利用されている著名なアルゴリズムを提供しています。コードは安定しており、長年にわたる検証を経ています。200 以上のテクニカル指標をサポートしており、API は C/C++ で記述されており Python ラッパー (wrapper) も提供されています。TA-Lib は BSD License (BSD-2-Clause license) の元で配布されているオープンソースのライブラリです。

以前は Linux 上で TA-Lib の Python 用パッケージを pip でインストールしてもビルドが必要で、しかもエラーでビルドできませんでした。自力でエラーを解決できなかったので TA-Lib の利用を避けていました。しかし最近の TA-Lib のバージョンの Python 用パッケージでは難なくインストールできることが判りました。

そこで今更ですが TA-Lib の使い方をおぼえようと、Jupyter Lab 上でテクニカル指標のいくつかをプロットしてみたので、備忘録的に内容をまとめました。

下記の OS 環境で動作確認をしています。

|

Fedora Linux Workstation |

42 x86_64 |

| Python |

3.13.7 |

| JupyterLab |

4.4.7 |

| matplotlib |

3.10.6 |

| mplfinance |

0.12.10b0 |

| numpy |

2.3.3 |

| pandas |

2.3.2 |

| ta-lib |

0.6.7 |

| yfinance |

0.2.65 |

サンプル

ライブラリをインポート

最初に利用するライブラリをまとめてインポートします。

import matplotlib.font_manager as fm

import matplotlib.pyplot as plt

import mplfinance as mpf

import numpy as np

import pandas as pd

import yfinance as yf

from talib import BBANDS, MACD, MFI, MOM, OBV, RSI, SAR, STOCH

yfinance で日経平均株価指数の過去データを取得

サンプルとして、今年の 1 月から半年間の日足データを取得します。

symbol = "^N225"

ticker = yf.Ticker(symbol)

df = ticker.history(start="2025-01-01", end="2025-07-01", interval="1d")

サンプル期間より少し古いデータからも取得しておきます。これでテクニカル指標を算出して、サンプルの期間の最初から指標がプロットされるようにします。

df2 = ticker.history(start="2024-10-01", end="2025-07-01", interval="1d")

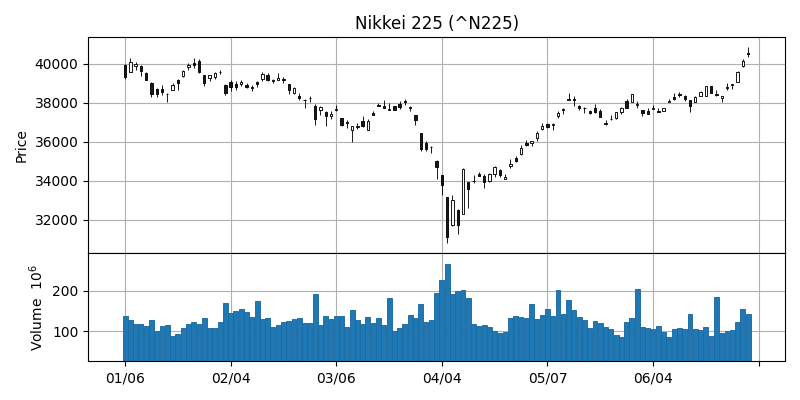

mplfinance でチャートを作成

サンプル期間の日足データをローソク足チャートと出来高の棒グラフを並べてプロットしました。

fig = plt.figure(figsize=(8, 4))

ax = dict()

n = 2

gs = fig.add_gridspec(

n, 1, wspace=0.0, hspace=0.0, height_ratios=[3 if i == 0 else 1 for i in range(n)]

)

for i, axis in enumerate(gs.subplots(sharex="col")):

ax[i] = axis

ax[i].grid()

mpf.plot(

df,

type="candle",

style="default",

datetime_format="%m/%d",

xrotation=0,

ax=ax[0],

volume=ax[1],

)

ax[0].set_title(f"{ticker.info['longName']} ({symbol})")

plt.tight_layout()

# plt.savefig("screenshots/n225_default.png")

plt.show()

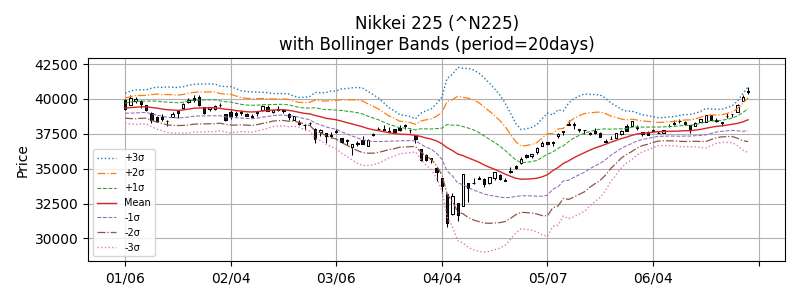

Bollinger bands

過去 20 日間の移動平均、移動標準偏差 +3σ, +2σ, +1σ, mean, -1σ, -2σ, -3σ でボリンジャーバンドを作成しました。

fig, ax = plt.subplots(figsize=(8, 3))

# BBANDS - Bollinger Bands

# upperband, middleband, lowerband = BBANDS(real, timeperiod=5, nbdevup=2, nbdevdn=2, matype=0)

period = 20

mv_upper_1, mv_mean, mv_lower_1 = BBANDS(df2["Close"], period, 1, 1)

mv_upper_2, _, mv_lower_2 = BBANDS(df2["Close"], period, 2, 2)

mv_upper_3, _, mv_lower_3 = BBANDS(df2["Close"], period, 3, 3)

apds = [

mpf.make_addplot(

mv_upper_3[df.index],

width=1,

color="C0",

linestyle="dotted",

label="+3σ",

ax=ax,

),

mpf.make_addplot(

mv_upper_2[df.index],

width=0.9,

color="C1",

linestyle="dashdot",

label="+2σ",

ax=ax,

),

mpf.make_addplot(

mv_upper_1[df.index],

width=0.75,

color="C2",

linestyle="dashed",

label="+1σ",

ax=ax,

),

mpf.make_addplot(

mv_mean[df.index],

width=1,

color="C3",

linestyle="solid",

label="Mean",

ax=ax,

),

mpf.make_addplot(

mv_lower_1[df.index],

width=0.75,

color="C4",

linestyle="dashed",

label="-1σ",

ax=ax,

),

mpf.make_addplot(

mv_lower_2[df.index],

width=0.9,

color="C5",

linestyle="dashdot",

label="-2σ",

ax=ax,

),

mpf.make_addplot(

mv_lower_3[df.index],

width=1,

color="C6",

linestyle="dotted",

label="-3σ",

ax=ax,

),

]

mpf.plot(

df,

type="candle",

style="default",

addplot=apds,

datetime_format="%m/%d",

xrotation=0,

update_width_config=dict(candle_linewidth=0.75),

ax=ax,

)

ax.grid()

ax.legend(fontsize=7)

ax.set_title(

f"{ticker.info['longName']} ({symbol})\nwith Bollinger Bands (period={period}days)"

)

plt.tight_layout()

# plt.savefig("screenshots/n225_talib_bbands.png")

plt.show()

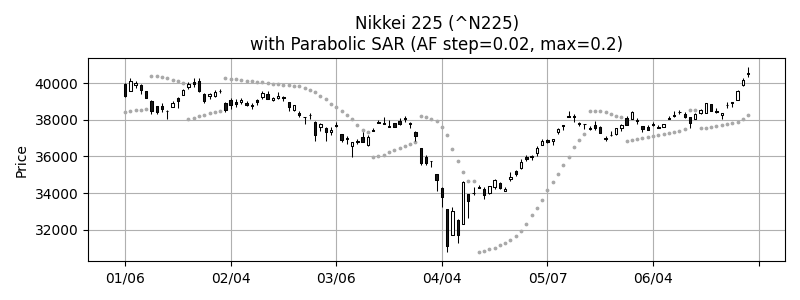

Parabolic SAR

AF step=0.02, max=0.2 で Parabolic SAR をプロットしました。上昇下降トレンドの情報が無いので、灰色の丸点でプロットしました。

fig, ax = plt.subplots(figsize=(8, 3))

# SAR - Parabolic SAR

# real = SAR(high, low, acceleration=0, maximum=0)

af_step = 0.02

af_max = 0.2

sar = SAR(df2["High"], df2["Low"], af_step, af_max)

apds = [

mpf.make_addplot(

sar[df.index],

type="scatter",

marker='o',

markersize=3,

color="darkgray",

ax=ax,

),

]

mpf.plot(

df,

type="candle",

style="default",

addplot=apds,

datetime_format="%m/%d",

xrotation=0,

update_width_config=dict(candle_linewidth=0.75),

ax=ax,

)

ax.grid()

ax.set_title(

f"{ticker.info['longName']} ({symbol})\nwith Parabolic SAR (AF step={af_step}, max={af_max})"

)

plt.tight_layout()

# plt.savefig("screenshots/n225_talib_sar.png")

plt.show()

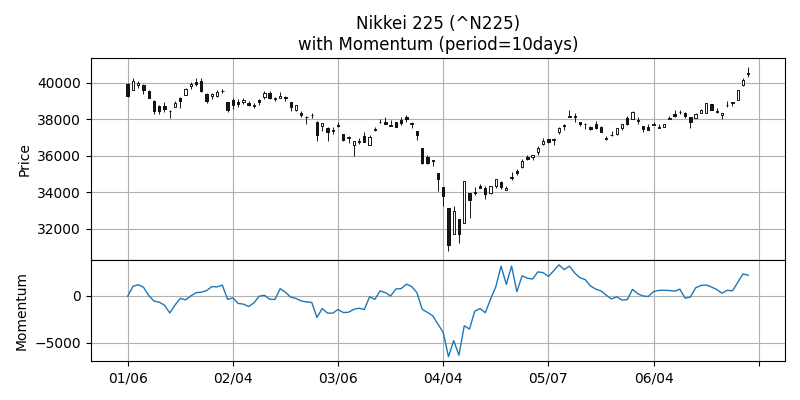

Momentum

過去 10 日間のデータでモメンタムを算出しました。

fig = plt.figure(figsize=(8, 4))

ax = dict()

n = 2

gs = fig.add_gridspec(

n, 1, wspace=0.0, hspace=0.0, height_ratios=[2 if i == 0 else 1 for i in range(n)]

)

for i, axis in enumerate(gs.subplots(sharex="col")):

ax[i] = axis

ax[i].grid()

# MOM - Momentum

# real = MOM(real, timeperiod=10)

period = 10

mom = MOM(df2["Close"], period)

apds = [

mpf.make_addplot(

mom[df.index],

width=1,

color="C0",

linestyle="solid",

ax=ax[1],

),

]

mpf.plot(

df,

type="candle",

style="default",

addplot=apds,

datetime_format="%m/%d",

xrotation=0,

ax=ax[0],

)

ax[1].set_ylabel("Momentum")

ax[0].set_title(

f"{ticker.info['longName']} ({symbol})\nwith Momentum (period={period}days)"

)

plt.tight_layout()

# plt.savefig("screenshots/n225_talib_mom.png")

plt.show()

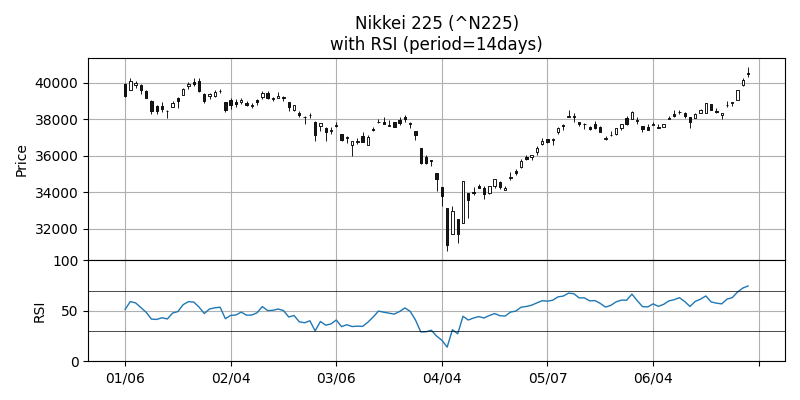

RSI, Relative Strength Index

過去 14 日間のデータで RSI を算出しました。

fig = plt.figure(figsize=(8, 4))

ax = dict()

n = 2

gs = fig.add_gridspec(

n, 1, wspace=0.0, hspace=0.0, height_ratios=[2 if i == 0 else 1 for i in range(n)]

)

for i, axis in enumerate(gs.subplots(sharex="col")):

ax[i] = axis

ax[i].grid()

# RSI - Relative Strength Index

# real = RSI(real, timeperiod=14)

period = 14

rsi = RSI(df2["Close"], period)

apds = [

mpf.make_addplot(

rsi[df.index],

width=1,

color="C0",

linestyle="solid",

ax=ax[1],

),

]

mpf.plot(

df,

type="candle",

style="default",

addplot=apds,

datetime_format="%m/%d",

xrotation=0,

ax=ax[0],

)

ax[0].set_title(f"{ticker.info['longName']} ({symbol})\nwith RSI (period={period}days)")

ax[1].set_ylabel("RSI")

ax[1].set_ylim(0, 100)

ax[1].axhline(30, color="black", linewidth=0.5)

ax[1].axhline(70, color="black", linewidth=0.5)

plt.tight_layout()

# plt.savefig("screenshots/n225_talib_rsi.png")

plt.show()

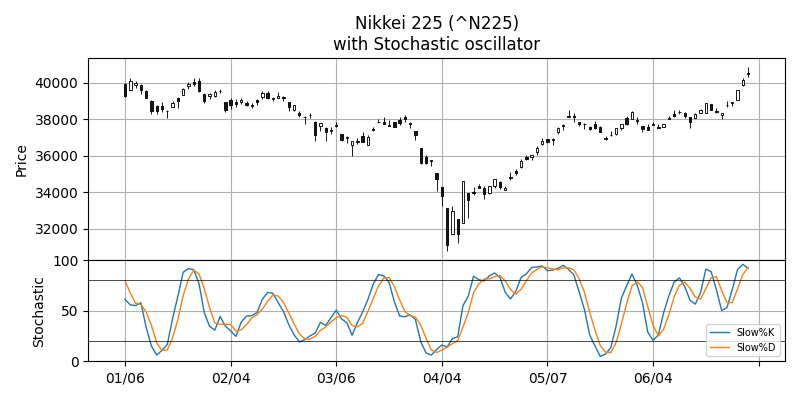

Stochastic oscillator

スローストキャスティクスをデフォルトのパラメータのままでプロットしています。

fig = plt.figure(figsize=(8, 4))

ax = dict()

n = 2

gs = fig.add_gridspec(

n, 1, wspace=0.0, hspace=0.0, height_ratios=[2 if i == 0 else 1 for i in range(n)]

)

for i, axis in enumerate(gs.subplots(sharex="col")):

ax[i] = axis

ax[i].grid()

# STOCH - Stochastic

# slowk, slowd = STOCH(high, low, close, fastk_period=5, slowk_period=3, slowk_matype=0, slowd_period=3, slowd_matype=0)

slowk, slowd = STOCH(df2["High"], df2["Low"], df2["Close"])

apds = [

mpf.make_addplot(

slowk[df.index],

width=1,

color="C0",

linestyle="solid",

label="Slow%K",

ax=ax[1],

),

mpf.make_addplot(

slowd[df.index],

width=1,

color="C1",

linestyle="solid",

label="Slow%D",

ax=ax[1],

),

]

mpf.plot(

df,

type="candle",

style="default",

addplot=apds,

datetime_format="%m/%d",

xrotation=0,

ax=ax[0],

)

ax[0].set_title(f"{ticker.info['longName']} ({symbol})\nwith Stochastic oscillator")

ax[1].set_ylabel("Stochastic")

ax[1].set_ylim(0, 100)

ax[1].axhline(20, color="black", linewidth=0.5)

ax[1].axhline(80, color="black", linewidth=0.5)

ax[1].legend(fontsize=7)

plt.tight_layout()

# plt.savefig("screenshots/n225_talib_stoch.png")

plt.show()

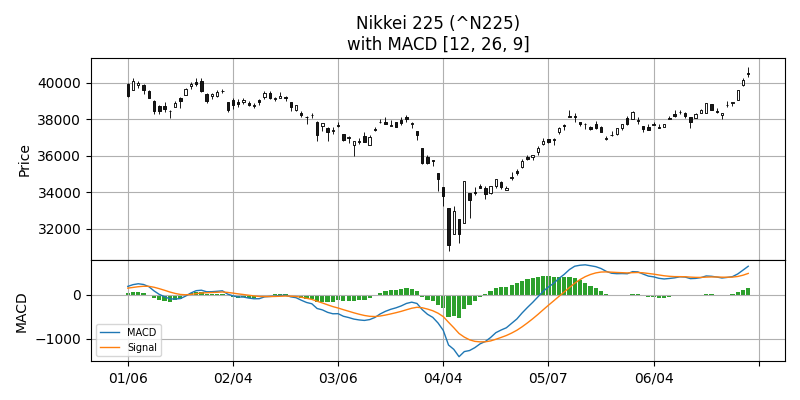

MACD, Moving Average Convergence Divergence

MACD もデフォルトのパラメータでプロットしています。MACD のヒストグラムは正負で色を変えたかったのですが、すぐに出来なかったので単色にしてしまいました。

fig = plt.figure(figsize=(8, 4))

ax = dict()

n = 2

gs = fig.add_gridspec(

n, 1, wspace=0.0, hspace=0.0, height_ratios=[2 if i == 0 else 1 for i in range(n)]

)

for i, axis in enumerate(gs.subplots(sharex="col")):

ax[i] = axis

ax[i].grid()

# MACD - Moving Average Convergence/Divergence

# macd, macdsignal, macdhist = MACD(real, fastperiod=12, slowperiod=26, signalperiod=9)

period_fast = 12

period_slow = 26

period_signal = 9

macd, signal, macdhist = MACD(df2["Close"], period_fast, period_slow, period_signal)

apds = [

mpf.make_addplot(

macd[df.index],

width=1,

color="C0",

linestyle="solid",

label="MACD",

ax=ax[1],

),

mpf.make_addplot(

signal[df.index],

width=1,

color="C1",

linestyle="solid",

label="Signal",

ax=ax[1],

),

mpf.make_addplot(

macdhist[df.index],

type="bar",

color="C2",

ax=ax[1],

),

]

mpf.plot(

df,

type="candle",

style="default",

addplot=apds,

datetime_format="%m/%d",

xrotation=0,

ax=ax[0],

)

ax[0].set_title(

f"{ticker.info['longName']} ({symbol})\nwith MACD [{period_fast}, {period_slow}, {period_signal}]"

)

ax[1].set_ylabel("MACD")

ax[1].legend(fontsize=7)

plt.tight_layout()

# plt.savefig("screenshots/n225_talib_macd.png")

plt.show()

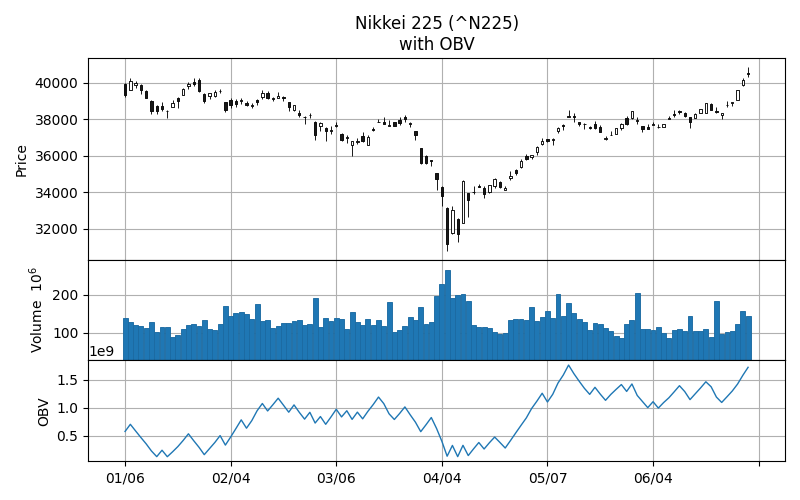

OBV, On Balance Volume

OBV は終値と出来高から算出する指標です。

fig = plt.figure(figsize=(8, 5))

ax = dict()

n = 3

gs = fig.add_gridspec(

n, 1, wspace=0.0, hspace=0.0, height_ratios=[2 if i == 0 else 1 for i in range(n)]

)

for i, axis in enumerate(gs.subplots(sharex="col")):

ax[i] = axis

ax[i].grid()

# OBV - On Balance Volume

# real = OBV(close, volume)

obv = OBV(df2["Close"], df2["Volume"])

apds = [

mpf.make_addplot(

obv[df.index],

width=1,

color="C0",

linestyle="solid",

ax=ax[2],

),

]

mpf.plot(

df,

type="candle",

style="default",

addplot=apds,

datetime_format="%m/%d",

xrotation=0,

ax=ax[0],

volume=ax[1],

)

ax[0].set_title(f"{ticker.info['longName']} ({symbol})\nwith OBV")

ax[2].set_ylabel("OBV")

plt.tight_layout()

# plt.savefig("screenshots/n225_talib_obv.png")

plt.show()

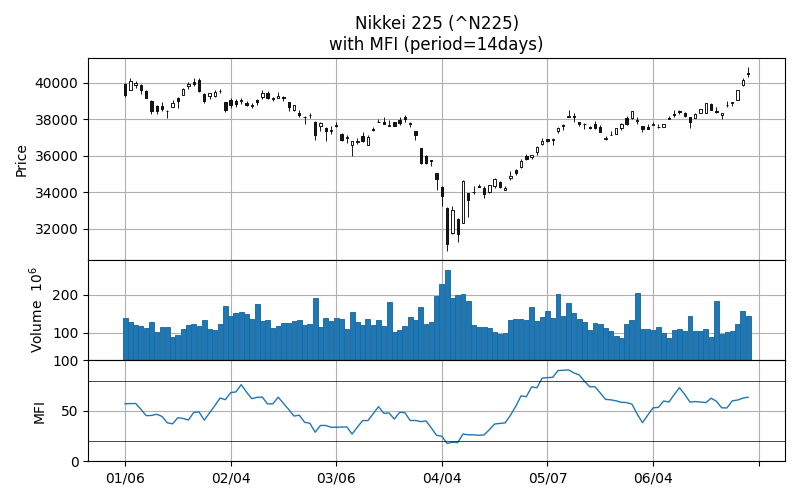

MFI, Money Flow Index

MFI も、株価と出来高から算出する指標です。

fig = plt.figure(figsize=(8, 5))

ax = dict()

n = 3

gs = fig.add_gridspec(

n, 1, wspace=0.0, hspace=0.0, height_ratios=[2 if i == 0 else 1 for i in range(n)]

)

for i, axis in enumerate(gs.subplots(sharex="col")):

ax[i] = axis

ax[i].grid()

# MFI - Money Flow Index

# NOTE: The MFI function has an unstable period.

# real = MFI(high, low, close, volume, timeperiod=14)

period = 14

mfi = MFI(df2["High"], df2["Low"], df2["Close"], df2["Volume"], period)

apds = [

mpf.make_addplot(

mfi[df.index],

width=1,

color="C0",

linestyle="solid",

ax=ax[2],

),

]

mpf.plot(

df,

type="candle",

style="default",

addplot=apds,

datetime_format="%m/%d",

xrotation=0,

ax=ax[0],

volume=ax[1],

)

ax[0].set_title(f"{ticker.info['longName']} ({symbol})\nwith MFI (period={period}days)")

ax[2].axhline(20, color="black", linewidth=0.5)

ax[2].axhline(80, color="black", linewidth=0.5)

ax[2].set_ylabel("MFI")

ax[2].set_ylim(0, 100)

plt.tight_layout()

# plt.savefig("screenshots/n225_talib_mfi.png")

plt.show()

参考サイト

- TA-Lib - Technical Analysis Library

- TA-Lib/ta-lib: TA-Lib (Core C Library)

- TA-Lib/ta-lib-python: Python wrapper for TA-Lib

- TA-Lib · PyPI

にほんブログ村

にほんブログ村

#オープンソース

#オープンソース